Forbearance and pandemic cash are operating out. However everybody had enjoyable.

By Wolf Richter for WOLF STREET.

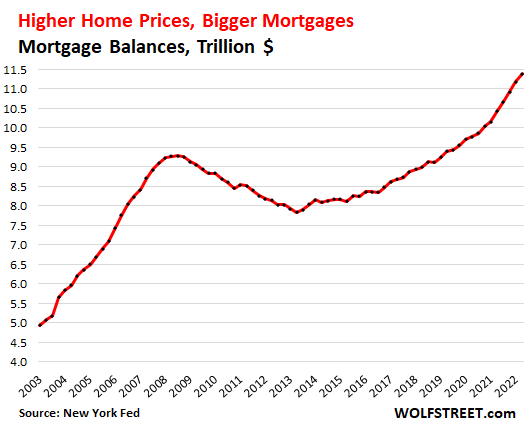

Mortgage balances jumped 9% within the second quarter from a yr in the past as costs climbed year-on-year as folks purchased far fewer properties – residence gross sales Present properties fell 10% from the second quarter of final yr and gross sales of recent single-family properties fell 19% over the identical interval.

Mortgage balances have risen relentlessly because the finish of the housing disaster in 2012. In these 10 years, mortgage balances jumped $4.6 trillion, and previously three years, mortgage balances jumped $2.0 trillion, or 21%, to $11.4 trillion.

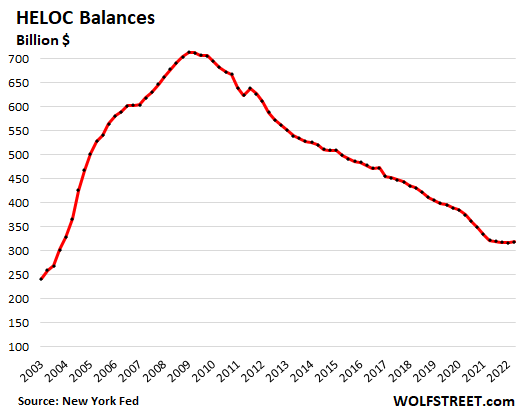

HELOCs finish an extended decline.

House fairness strains of credit score fell out of favor after 2009 and balances steadily declined, reversing the huge surge of the years earlier than the monetary disaster. Because the Fed’s rate of interest crackdown and QE drove mortgage charges down and home costs rose, folks started to money out and refinance their mortgages to generate money, slightly than to faucet into the HELOCs.

However now the decline is over. HELOC balances rose within the second quarter to $319 billion, from the earlier quarter’s low. It got here as mortgage charges soared and money remittances plunged.

Now there’s a new dynamic in place: A lot increased mortgage charges: It might be silly to refinance a 3% mortgage with a 5% mortgage in an effort to get $100,000 money out of the home. It is best to go away the three% mortgage alone and get a $100,000 HELOC that expenses 5% on the excellent stability, if any. So I count on HELOC balances to extend additional sooner or later because the cash-in refi recreation has modified.

Mortgages are by far the biggest a part of client debt, larger than ever.

Nothing even comes shut. Q2 Client Debt Balances:

- Mortgages: $11.4 trillion

- Pupil loans: $1.6 trillion

- Auto loans: $1.5 trillion

- Bank cards: $890 billion

- “Different” (private loans, and many others.): $470 billion

- HELOC: $320 billion.

Mortgages are the place the massive systemic dangers was once as a result of sheer measurement of the market and excessive leverage.

However now, industrial banks in the USA solely maintain about $2.4 trillion in residential mortgages, together with HELOCs, on their stability sheets, and people are unfold throughout 4,300 industrial banks. 1000’s of credit score unions and different lenders additionally maintain mortgages on their stability sheets.

However most mortgages are actually securitized into mortgage-backed securities. MBS are divided into two classes:

- Most are government-backed MBS. Right here the taxpayer is accountable, not the traders and lenders.

- A smaller portion of MBS are “non-public manufacturers” – not backed by authorities entities. They’re held by international bond funds, pension funds, insurance coverage firms, and many others.

Crimes are beginning to come again to actuality. Everybody had enjoyable.

Beneath pandemic-era forbearance applications, owners who fell behind on their mortgage funds, or stopped making mortgage funds altogether after which entered a forbearance program, had been reclassified as “present” as a substitute of delinquent. They did not should make mortgage funds and will use the cash saved from these unpaid mortgage funds for different issues. Finally, they must attain an settlement with the lender to exit the forbearance program.

The surge in residence costs because the spring of 2020 has allowed owners, upon exiting the forbearance program, to promote the house and repay the mortgage and stroll away with additional money; or make a cope with the lender, resembling a modified mortgage with a long run, decrease charge, and decrease funds. And everybody had enjoyable.

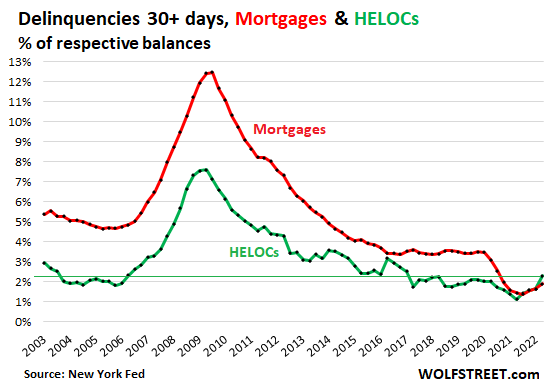

However with the tip of forbearance applications, mortgage delinquencies have began to rise this yr from final yr’s file highs.

Mortgage balances that had been 30 days or extra late reached 1.9% of complete mortgage balances within the second quarter, in comparison with 1.7% within the first quarter. It was the third consecutive quarter-over-quarter improve, from the file low within the second quarter of 2021. However it stays under all pre-pandemic lows (purple line).

HELOC gross sales which had been 30 days or extra late reached 2.3% of complete HELOC balances, the fourth consecutive quarter-over-quarter improve, from the file low within the second quarter of 2021. They’re now increased than they had been earlier than the housing disaster (inexperienced line).

The HELOC delinquency charge within the second quarter was increased than the mortgage delinquency charge for the very first time, making you go hmmm.

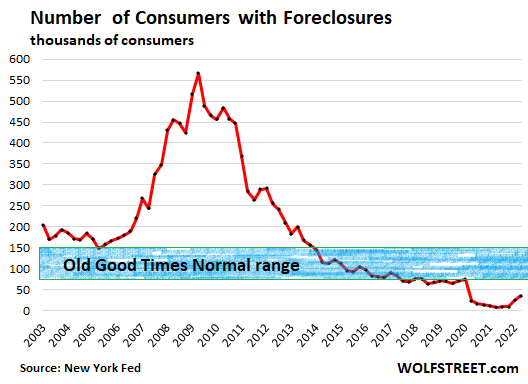

Seizures have elevated, however are nonetheless close to all-time lows.

The variety of foreclosed shoppers rose to 35,120 debtors from 24,240 within the first quarter and from the file vary of 8,100 to 9,600 final yr.

Foreclosures are nonetheless nicely under pre-pandemic lows. On the low of Q2 2005, throughout the Better of Occasions simply earlier than the Housing Bust took off, there have been 148,780 foreclosures, greater than 4 instances as a lot as now.

As compared, throughout the three-year interval from 2008 to 2011, the height of the mortgage disaster, greater than 400,000 shoppers per quarter had been topic to foreclosures, together with 566,180 on the peak of the second quarter of 2009.

Throughout the perfect of instances earlier than the housing disaster, about 150,000 shoppers had foreclosures; and throughout the good instances earlier than the pandemic, about 75,000 shoppers had seizures per quarter. This vary of 75,000 to 150,000 seizures might signify one thing just like the outdated Good Occasions Regular (blue field), and we’re not there but:

Home costs and foreclosures.

A spike in foreclosures can solely occur if there’s a drop in home costs. When a home-owner who purchased the home two years in the past for $400,000 is in hassle now, when the worth of the home has jumped 25% to $500,000, he can merely promote the home, repay the mortgage, pay the charges and stroll away with the cash left over. And there might be no foreclosures.

If the worth of that home in the end drops 25% to $375,000 and the borrower owes $390,000 on the mortgage, that exit turns into harder.

If the worth dips 40% to $300,000, the simple exit is closed. That is when foreclosures begin to occur in massive numbers, particularly if accompanied by a pointy rise in unemployment, and that is what occurred throughout the mortgage disaster. However it’s not on the desk but.

Do you prefer to learn WOLF STREET and need to help it? You utilize advert blockers – I utterly perceive why – however you need to help the positioning? You may donate. I significantly admire it. Click on on the mug of beer and iced tea to learn how:

Would you prefer to be notified by e-mail when WOLF STREET publishes a brand new article? Register right here.

![]()

#journey #actuality #begins #mortgages #HELOCs #defaults #foreclosures #quarter